KrisFlyer miles aren’t always easy to come by. Apart from those flying regularly with Singapore Airlines or their Star Alliance partners, usually for work and often in premium classes, the majority of us rack up the bulk of our miles from our monthly credit card spending.

Luckily there are some generous miles earning rates out there on several credit cards issued in Singapore, so it’s likely you’re earning 1 to 1.4 miles per S$1 spent locally, and 2 to 3 miles per S$1 spent overseas.

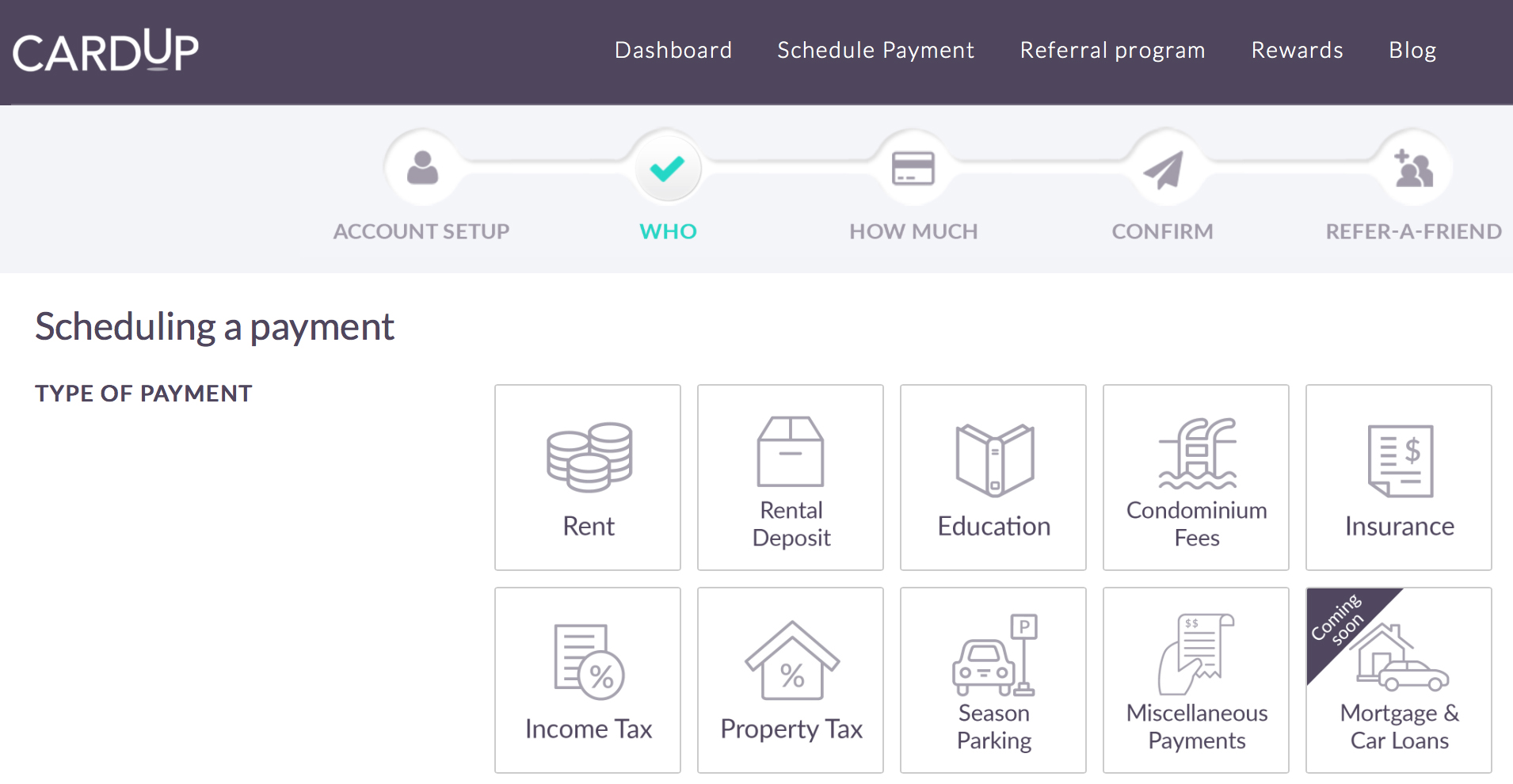

It can add up to a lot of points over the year, but annoyingly you can’t use your card for some of life’s biggest expenses, like rent payments, school tuition fees and insurance premiums, right? Wrong! This is where CardUp comes in…

The deal

For a 2.6% processing fee, CardUp allows you to pay many of these expenses using your credit card, and you’ll get all the usual points and miles awarded for the transaction, just as though you were making the payment directly.

The process is relatively simple:

- sign up (your landlord or recipient doesn’t have to)

- add your credit card(s), either local or overseas, then

- schedule your payments

Payments can be one-off or recurring, like your monthly rent. All major Visa and MasterCard credit cards are accepted, and they can be overseas cards too if that works better for you.

Is it worth it?

This depends on two things:

- the miles earning rate associated with your card, and

- what a KrisFlyer mile is worth to you.

I currently pay my monthly rent through CardUp, using my Standard Chartered Visa Infinite card, which earns 1.4 miles per S$1 spent locally. So where previously I was paying $4,000 a month directly to the landlord, I now pay $4,104 a month to CardUp, then they pay the landlord on my behalf.

So it’s costing me $104 a month extra (the 2.6% fee), which isn’t a negligible amount, however previously I was earning no KrisFlyer miles at all from paying my rent, now I am earning 5,745 miles a month (4,104 x 1.4). That effectively means I’m paying S$0.0181 (1.81 cents) per KrisFlyer mile.

As we explained in our article how much is a KrisFlyer mile worth, we conservatively value KrisFlyer miles at about 2 cents each. Unless you exclusively redeem in economy, which isn’t where the true value of the miles lies, it’s what you’ll realistically and easily achieve for a good spread of redemptions.

As the article goes on to state, we tend to achieve closer to 3 cents per mile in value from the miles we use, so we have a personal upper limit to buy of 2 cents per mile, to allow sufficient buffer for the fact that miles are not as flexible as cash (redemptions aren’t always available), and to protect against any future devaluation of the scheme.

It’s easy to achieve more than 2 cents per mile, particularly if you use your miles for long haul business class redemptions (and especially for those of us who would only consider travelling in business on a long sector, such as from Singapore to Europe or the USA, as the value of the miles is then ‘true’).

But we think you certainly won’t lose money assuming a 2-cent valuation, so ‘buying’ the miles as you are doing here with CardUp for 1.81 cents, while not the best deal in the world, is still a good deal in our opinion.

Let’s say however that your card only gives you 1.2 miles per S$ spent locally, the maths now shows you’re ‘buying’ the miles for 2.11 cents each. We probably wouldn’t buy at that price, so unless you know you can achieve a significantly better than a 2 cent return from your miles, or you’re topping-up your miles balance towards something specific in the near future, we wouldn’t recommend buying at this rate.

To some extent it’s also a personal calculation based on what difference this many more miles can make to your account. If you’re hopping around the world in business class at your company’s expense, and you put your regular spending on a decent miles-earning credit card, chances are you aren’t short of KrisFlyer miles (I know several people running balances of well over 1 million). For them, it probably isn’t worth using CardUp to ‘pay’ for more miles.

If you’re a small-time collector by comparison though, CardUp may give you the opportunity to significantly increase your miles pot each year. In the case of my own condo rental, it’s nearly an extra 69,000 miles a year alone. If your regular earning would otherwise be say 50,000 per year, that’s a massive difference and opens up many redemption opportunities you may not have previously had access to, such as business class redemptions to Europe.

In this case topping up your miles by buying them at or slightly above 2 cents per mile may make sense for you. Remember though, there are other ways to ‘buy’ KrisFlyer miles for less than that which you should try to exploit first.

Is it legitimate?

Absolutely. I’ve been using CardUp for many months and the payments to my landlord have been seamless. Notifications are provided when the money is taken from your credit card and each time it is credited to the recipient.

You can easily log on to view, amend or cancel scheduled payments, or swap the card you are using for any particular payment (or all future ones).

Won’t the banks put a stop to this?

You’d think the banks issuing these credit cards in Singapore would be rather unhappy about having to dish out such a large volume of points and miles to their customers using a ‘loophole’ like this.

In fact, the opposite is true. CardUp is actually currently working with UOB to promote the service with a special offer allowing you to earn 2.4 miles per $1 spent with CardUp, if you sign up for their PRVI Miles card, up to the first 40,000 miles earned by 31 December, then reverting to 1.6 miles per $1.

That’s effectively ‘buying’ KrisFlyer miles for 1.08 cents each at the higher rate, reverting to 1.63 cents per mile after that, a very attractive rate, and seemingly with the bank’s full endorsement.

You don’t have to credit to KrisFlyer

As the credit card points you will earn from your CardUp payments are the regular ones associated with your credit card rewards scheme, you are free to transfer the points into miles not only with KrisFlyer, but any other scheme your card provider allows.

For example, I earn 1.4 miles per $1 spent with my Standard Chartered card, but I have to credit the points into KrisFlyer miles. With my Citi PremierMiles card I earn 1.2 miles per $1 spent, but there’s a list of 10 other airline frequent flyer programs to transfer into, plus some hotel schemes like IHG and Hilton.

If I need a quick top-up of miles in a different frequent flyer scheme, I can just switch my payment next month to the Citi card.

Is American Express accepted?

Not at this time, and not too surprisingly, as it’s widely known AMEX merchant transaction fees are some 50% higher than Visa or MasterCard charge (typically 3%, rather than 2%).

If you walk into a store anywhere in the world, and there’s a card they don’t accept, it’s likely to be AMEX rather than any of the other major issuers, due to these higher fees. The reason there are many stores that do accept American Express, and so are willing to swallow the extra charges, is that the AMEX customer base tends to be more affluent consumers, who are very attractive to merchants.

However, this wouldn’t help a company like CardUp, who only exist to take advantage of the margin between the fee they pay the card issuer, and the fee they charge you for the advantage of being able to pay a bill which wouldn’t otherwise be possible with a credit card.

Are there any other companies doing this?

Yes, CardUp wasn’t actually the first to get in on the game in Singapore. ipaymy actually started offering the service first, back in early 2016. They were initially offering the same service for a higher fee of between 2.75% and 2.95%, depending on your monthly rent amount, but since CardUp established they too matched the 2.6% charge, and fundamentally provide the same services.

Sign up for CardUp here using our referral code MAINLYMILES and you’ll get S$20 credit towards your first payment.

Mainly Miles has no particular affiliation with one provider or the other, and I simply chose to write about CardUp because this is the company I am personally using to take advantage of this miles-boosting option.

Andrew, you mention the cardup and UOB promo which the link still has details for signing up before December 2017. Is the preferential rate (if not the higher rate) of 1.6 still available for UOB card members if I was to sign up now with my new UOB PRVI miles card?

That particular offer has expired unfortunately so currently you’ll just get the regular rate through UOB PRVI Miles. If something else comes up we’ll be sure to write about it.