The last few months have represented a bumper time for offers in the card payments field here in Singapore. Not only have companies like CardUp and ipaymy been continuing to offer customers the ability to earn miles using their credit card for bills like rental, income tax, education and home improvement invoices, but at the same time banks have been getting in on the act too.

UOB were already well established with their PRVI Pay option, available to PRVI Miles cardholders since 2017 and touted as temporary but never actually discontinued. Recently they hiked the 2% fee slightly to 2.1%, but also threw out a promotional 1.8% offer to selected cardholders in June 2019, with another offer for all customers at the original 2% fee for August and September 2019.

![]()

Citi were next to join the field with PayAll, tested with selected users from just 1.2% fee, then rolled out at a 1.5% or 2% fee but more recently settling at the 2% rate for all users.

![]()

A few months ago OCBC joined the realm with their Voyage Payment Facility, allowing Voyage credit cardholders to make effectively unlimited payments for a 1.95% fee (1.9% for very large payments in excess of S$150,000). The downside there – a minimum S$10,000 payment amount applies.

The new kid on the block

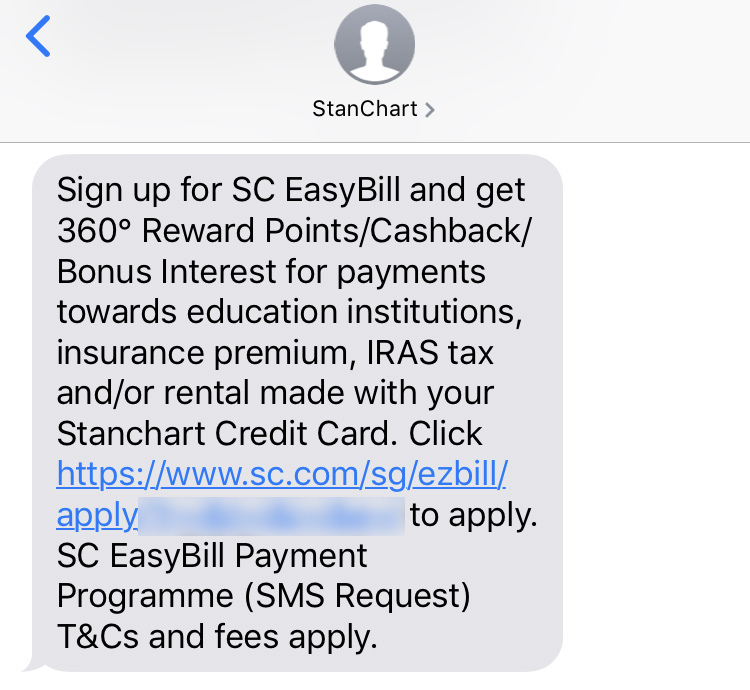

This week Standard Chartered jumped on the bandwagon with EasyBill, a way for their credit card customers to earn the usual rewards points or cashback for outgoings not usually allowing credit card payments, like rental and education expenses.

![]()

In fact EasyBill was initially targeted to selected customers a couple of months ago, but since 6th August 2019 the EasyBill feature now appears on all credit card landing pages on the Standard Chartered website, including for the new X card.

To make an EasyBill payment you’ll first have to send an SMS to Standard Chartered from the same mobile number as your registered account(s) with the bank.

Standard Chartered will then reply with a URL for you to use to set up you payment. The bad news is if the SMS reply does not contain the URL to the Online Application, you are not eligible for EasyBill on the basis of the bank’s own “internal review processes and policies”.

Assuming you are eligible (both Eddie and I received the URL link in the SMS reply), you will then be shown at the online application form stage what fee will be charged for your transaction type.

The fee

Standard Chartered say “The SC EasyBill Fee is not a fixed amount as it will vary according to the SC EasyBill Facility chosen by the Qualified Cardholder in the Online Application. The SC EasyBill Fee may be changed at any given time as per the Bank’s discretion.”

In fact for both Eddie and I the fee charged is 2% regardless of payment type selected.

We suspect this is the standard offer but please let us know if you’ve been targeted for a different rate.

Payment types

EasyBill supports the following payment types:

- Rent

Payments towards the monthly rental amount specified in a tenancy agreement as entered into between you and your landlord. - IRAS

Payments made towards the Inland Revenue Authority of Singapore for individual tax or property tax purposes. - Insurance

Insurance premium payments due towards any insurance policies including health insurance, motor insurance, life insurance, foreign domestic worker insurance and travel insurance. - Education

Payments towards any educational service like school fees, university fees, polytechnic fees, fees related to training institutes, for enrichment centres and day cares, pertaining to extracurricular activities (e.g. dance, music, painting, cookery, yoga, gardening, language programmes), fees for hobbies, for any sports activity involving an instructor, and tuition fees.

SC EasyBill currently only supports one-time payment requests and not recurring payments. That’s especially inconvenient for rental payments, as you’ll have to set up a new payment each month, so hopefully it’s a feature that will be added in future.

How it works

Once you follow the eligible payment link from your SMS, you can select your payment type and the fee charged will be shown.

After that fill in the required details, for example the following image shows a S$5,000 rental payment to a landlord.

In one of the fields you’ll be asked to enter your Standard Chartered credit card number, so if like me you are holding both the SCVI and the X card this is where you will be able to specify which card the EasyBill transaction will be charged to and which one will accrue reward points.

The applicable fee is shown before you proceed (S$100 / S$5,000 = 2% in this example).

Note that to confirm your EasyBill payment you will not be asked up upload any supporting documents at this stage, such as an invoice or tenancy agreement, but that Standard Chartered may ask you to submit “documents evidencing that the transaction made using SC EasyBill is an Eligible Payment” before processing the application.

How long does it take?

Standard Chartered specify a 7 business day period from submission to payment date for an EasyBill transaction.

How are points awarded?

Most of our readers will be using EasyBill to accrue more rewards points to transfer into airline miles through their Visa Infinite card or X card, rather than the cashback or bonus interest offers available with some other products.

Points will be awarded at your regular local earn rate for the EasyBill amount:

- SC Visa Infinite: 3.5 rewards points per S$1 (1.4 mpd)

- SC X card: 3 rewards points per S$1 (1.2 mpd)

Bear in mind that to earn the enhanced 1.4 miles per dollar rate on your Standard Chartered Visa Infinite card, you’ll have to spend more than S$2,000 in the same statement cycle, though EasyBill payments are counted towards this. Otherwise you will earn 1 mile per dollar.

Bear in mind that the EasyBill fee will be listed separately on your statement, and the fee itself does not accrue any reward points.

What’s the cost per mile?

Cost per mile for SC EasyBill for the miles-earning cards comes out as follows, assuming a 2% fee:

| Card | Miles per S$1 | Cost per mile (2% fee) |

SC Visa Infinite SC Visa Infinite |

1.4 | 1.43¢ |

SCVI X card SCVI X card |

1.2 | 1.67¢ |

Cost per mile for the Standard Chartered Visa Infinite card assumes greater than S$2,000 total spend on the card in the same statement cycle, otherwise the lower earning rate of 1 mile per dollar brings the cost to (an unattractive) 2 cents per mile.

SCVI Income Tax Payment remains

One thing Standard Chartered Visa Infinite cardholders won’t want to use SC EasyBill for is an IRAS income tax payment, since that card still boasts the tax payment facility for a 1.6% processing fee.

This gives you a cost of 1.14 cents per mile, among the best deals on the market for income tax payment, provided your total spending is greater than S$2,000 during the same statement cycle to trigger the 1.4 mpd local earn rate.

SC EasyBill may still be useful however for IRAS property tax payments or other individual tax obligations with your SCVI card.

If your income tax bill is less than S$2,000 and you won’t make up the difference in the same statement cycle on your SCVI card with general spending, EasyBill actually comes in cheaper than the tax payment facility (1.43 cents per mile vs. 1.6 cents per mile).

The X card sign-up promotion

EasyBill payments do not count towards the S$6,000 minimum spend in the first 60 days of X card membership for the 100,000 miles or 60,000 miles sign-up bonus.

You will still earn the regular 1.2 miles per dollar for EasyBill transactions during this period (as you will for example with a CardUp or ipaymy transaction), but these categories are specifically excluded in the terms and conditions towards the S$6k minimum spend to trigger the sign-up bonus.

How does it compare?

Here are a few examples of options available to buy miles through your credit card for rental payments using some commonly held cards, including some ongoing promotions for the rest of 2019 like our MAINLYMILES185 code with RentHero.

| 2019 Rental payment | ||||

| Card | Method | Fee | Miles per S$1 |

Cost per mile |

| 1.89% | 1.6 | 1.16¢ | ||

| 1.9% | 1.6 | 1.17¢ | ||

| 2% | 1.6 | 1.25¢ | ||

| 1.85% | 1.5 | 1.21¢ | ||

| 1.89% | 1.5 | 1.24¢ | ||

| 1.9% | 1.5 | 1.24¢ | ||

| 1.85% | 1.4 | 1.30¢ | ||

| 1.89% | 1.4 | 1.32¢ | ||

| 1.9% | 1.4 | 1.33¢ | ||

| PRVI PAY | 2% | 1.4 | 1.43¢ | |

| 2% | 1.4 | 1.43¢ | ||

| 1.89% | 1.3 | 1.43¢ | ||

| 1.9% | 1.3 | 1.43¢ | ||

| 1.85% | 1.2 | 1.51¢ | ||

| 2% | 1.3 | 1.54¢ | ||

| 2% | 1.3 | 1.54¢ | ||

| 1.89% | 1.2 | 1.55¢ | ||

| 1.9% | 1.2 | 1.55¢ | ||

| 1.89% | 1.2 | 1.55¢ | ||

| 1.9% | 1.2 | 1.55¢ | ||

| 1.89% | 1.2 | 1.55¢ | ||

| 1.9% | 1.2 | 1.55¢ | ||

| 2% | 1.2 | 1.67¢ | ||

| 2% | 1.2 | 1.67¢ | ||

| 2.6% | 1.2 | 2.11¢ | ||

| 2.6% | 1.2 | 2.11¢ | ||

| 2.6% | 1.1 | 2.30¢ | ||

| 3.3% | 1.2 | 2.66¢ | ||

| 3.3% | 1.2 | 2.66¢ | ||

| 3.3% | 1.1 | 2.90¢ | ||

As you can see there are several cheaper options for rental payments alone with some popularly held cards on the market, including the UOB PRVI Miles and BOC Elite Miles options.

You’ll also get a better deal using your SCVI or X card with our RentHero promotional rate, or with both CardUp and ipaymy’s current rental offers, than you will using EasyBill. All of those alternatives also boast the recurring payments option, ideal for these monthly transactions.

Terms and conditions

The full terms and conditions for the EasyBill service are available here.

Summary

A couple of years ago only one bank, UOB, was offering a bill payment option for one of its credit cards. SC EasyBill now brings the total to four banks, with Citi and OCBC also offering similar facilities on at least one of their miles-earning credit cards.

EasyBill was initially trialled in June this year to selected users, however neither Eddie nor I were targeted. The fact that we are both now eligible to apply at a 2% transaction fee suggests this facility is now widely available to Standard Chartered credit card holders.

Remember EasyBill transactions do count towards the S$2,000 minimum spend per statement cycle on the SCVI card to trigger the enhanced 1.4 mpd local earn rate, but won’t count towards your S$6,000 minimum spend for the X card sign-up bonus promotion.

Before you sign up for EasyBill do check out the alternatives. Several credit cards on the market boast better rates through their own payment programs or through the likes of CardUp and ipaymy, especially for rental transactions with a wide range of competitive offers ongoing through the end of 2019.

We have updated our full review of the Standard Chartered Visa Infinite card to include details of the SC EasyBill facility.

Have you had SC EasyBill payments offered to you at a different fee than the ‘generic’ 2%? Have you used the facility and then been asked to provide supporting documents prior to approval? Let us know in the comments section below.

“If your income tax bill is less than S$2,000 and you won’t make up the difference in the same statement cycle on your SCVI card with general spending, EasyBill actually comes in cheaper than the tax payment facility (1.43 cents per mile vs. 1.6 cents per mile).”

If you spend less than $2k/MTH on SCVI, won’t the miles earned under EasyBill also drop to 1mpd (instead of 1.4mpd) as well? Then your cpm will be higher. That will mean the tax payment facility is still cheaper than EasyBill.

Ah ok what we mean is EasyBill on the X card will come out cheaper than SCVI tax payment in that case (assuming you have both cards).

Sorry if it’s not clear – will reword!

Thanks for the detailed analysis!

If we’re using Cardup to pay for insurance, where the fee is 2.6% (instead of 1.9% for rent) then it would appear EasyBill is a cheaper option.

Perhaps you can do another comparison table when you have time.

Cheers!