Here’s our review of the UOB Visa Signature (VS) card, which forms part of our series of credit card reviews, all of which are summarised on our dedicated Credit Cards page.

Dollar amounts refer to SGD, and ‘miles’ refer to KrisFlyer Miles, except where stated. This review was updated on 13th September 2020.

| Fast Facts

Annual fee: $214.00/yr (first year free) |

Annual fee

The annual fee for the UOB VS card is $214.00, however this is waived for the first card membership year.

Sign-up bonus

There is no current miles sign-up bonus for the UOB VS card, however new applicants between 1st March and 30th June 2020 are entitled to a $150 cash credit subject to a minimum spend of $1,500 within 30 days from the card approval date.

As usual with UOB, it’s limited to the first 800 new-to-bank cardholders to meet the spend threshold, so don’t count on getting it (they won’t even tell you if the promotion is fully taken up).

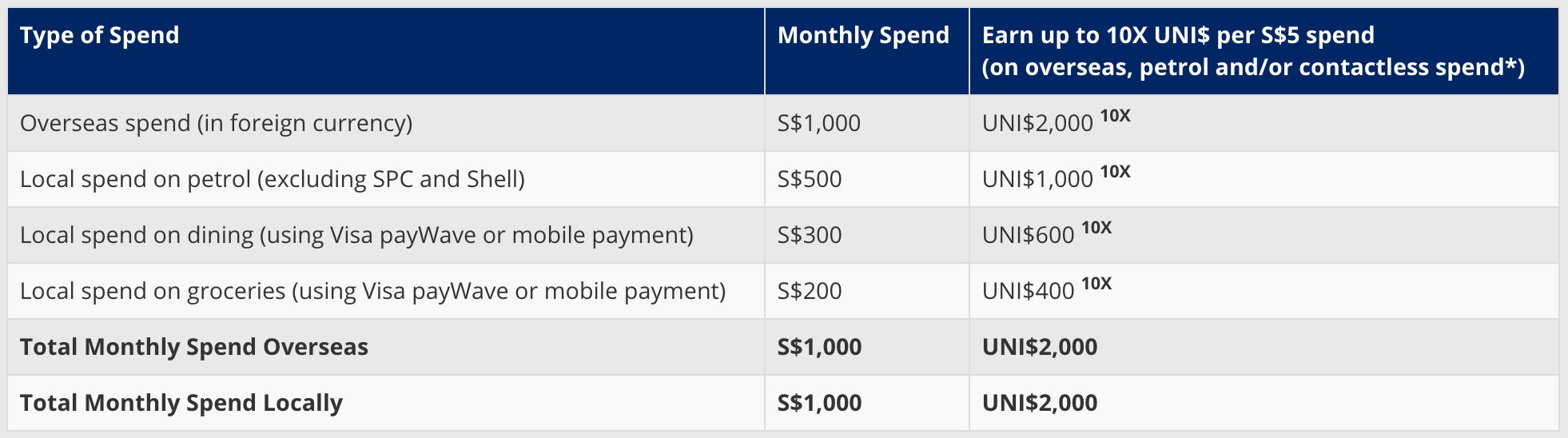

Earning rates

The UOB VS earns:

- 0.4 miles per dollar (1 UNI$ per $5) spent both locally and overseas (i.e. transacted in foreign currency)

- 4 miles per dollar (10 UNI$ per $5) spent on overseas transactions (i.e. in foreign currency), including online purchases in foreign currency, subject to a minimum spend of $1,000 in foreign currencies per statement period

- 4 miles per dollar (10 UNI$ per $5) spent on petrol purchases and all contactless transactions (Visa payWave or mobile device payments), subject to a minimum spend of $1,000 in local transactions per statement period

The 10 UNI$ consists of the basic $1 UNI$ earned plus an additional of 9 bonus UNI$. The

bonus UNI$ will be credited to you in the following statement period.

Both bonus 4 mpd categories are capped at a combined total of UNI$4,000 in each statement period ($2,000 spending).

Since most of our readers will be (rightly) disinterested in the lousy 0.4 mpd earn rate, there are some very important things to be aware of when it comes to the bonus 4 mpd levels:

- It’s statement period, not calendar month. Be careful to ensure that your minimum qualifying spend and the transactions you want to make at the enhanced rate will be posted to your account within the same statement. “UOB will not be liable for any late transaction postings affecting your eligibility to qualify for the bonus UNI$.”

- Each bonus category must be triggered to ‘activate’ that category’s enhanced earn rate. That’s $1,000 in overseas spend to activate the overseas spend bonus and $1,000 in local spend to activate the petrol / contactless bonus.

- If you’re activating the overseas transactions bonus category within your statement period, be careful to ensure you don’t transact in Singapore Dollars (i.e. DCC). Your payment must be processed in foreign currency. Also, online transactions in foreign currencies at merchants with their payment gateway in Singapore are not eligible.

Overseas transactions

The first category for the enhanced earn rate of 4 miles per dollar using the UOB VS card is for overseas transactions. Here’s how UOB outlines it:

“UNI$10 for every S$5 spent on transactions in foreign currencies, including online transactions in foreign currencies (with payment gateway outside Singapore), subject to a minimum foreign currencies spend of S$1,000 per statement period. Online transactions in Singapore Dollars or in foreign currencies at merchants with payment gateway in Singapore will earn UNI$1 for every S$5 spent.”

That covers the important bases we’ve already outlined, but in summary:

- Physical or online transactions in foreign currency

- Minimum $1,000 per statement period (maximum $2,000)

- Be careful not to inadvertently use DCC (i.e. pay in SGD)

- Be careful not to spend online in FCY at merchants with a payment gateway in Singapore

Petrol and contactless transactions

The second combined category for the enhanced earn rate of 4 miles per dollar using the UOB VS card is for petrol and contactless transactions. Here’s how UOB outlines it:

“UNI$10 for every S$5 spent on petrol (excluding SPC and Shell) and contactless transactions (excluding SMART$ merchants), subject to a minimum local spend of S$1,000 in total, per statement period”

In summary, with a minimum $1,000 local spend per statement period (maximum $2,000, shared cap with the overseas transactions above), you’ll get:

- 4 mpd on all petrol purchases (excl. SPC and Shell)

- 4 mpd on all contactless transactions, including mobile wallet transactions, but excluding SMART$ merchants

One of the more flexible benefits of the UOB VS card is the 4 miles per dollar rate on contactless (Visa payWave or mobile device payments).

Here’s how you can use it in this category, by either tapping the physical card or using the card saved through a mobile wallet:

|

Visa payWave |

|

Android Pay |

|

Samsung Pay |

|

Apple Pay |

Contactless transactions made overseas with your UOB VS card in foreign currency are included in the offer.

The second and crucial point is that payment must be made by physically waving your card or phone. Magnetic stripe transactions will not be eligible.

Note: UOB recently restricted its contactless transactions category using its PPV card to mobile contactless transactions only (e.g. using Apple Pay, Google Pay, Samsung Pay), with effect from 22nd May 2020, however there have been no announced changes to the contactless transactions with the UOB VS cards, which continue to support either mobile wallets or tapping the physical card when paying.

Be careful of SMART$

UOB partners with some retailers to offer SMART$ rather than UNI$. This is effectively a ‘cashback’ scheme, offering a means to offset your next purchase with accumulated SMART$.

Unfortunately, it overrides the UNI$ scheme. That means if you make a contactless in-store transaction at a retailer which is part of the SMART$ scheme (e.g. Visa payWave at a Cold Storage outlet), you won’t earn 4 miles per dollar for your transaction.

You can view a list of UOB SMART$ merchants here. Be careful of the following:

- Cathay Cineplexes

- Cold Storage

- Giant

- Guardian

- Jasons

- Marketplace

- Shell

Don’t use this card (e.g. via payWave) if you make a purchase at a merchant in this list, as you’ll get SMART$ instead of 4 miles per dollar.

Which bonus category to ‘choose’

Unless you’re going to spend almost exactly (and at least) $1,000 in each of the two 4 mpd bonus categories in the same statement period, it’s a much better strategy to stick to just one of them. Otherwise you may end up wasting spend at the 0.4 mpd rate in a category just to trigger the 4 mpd rate for the majority of it, diluting the overall earn rate.

Worse still, you might fall just short of activating one bonus category by mistake, rendering all the spend within that category to 0.4 mpd.

There are some common misconceptions for bonus miles earning with this card, so let’s try to address those with a few examples.

Example 1: Within the same statement period I spend $600 in overseas transactions and $600 on local (SGD) Visa payWave. Do I earn 4 mpd?

No – neither bonus category was ‘activated’ in the same statement period, so you’ll earn 0.4 mpd for everything.

Example 2: Within the statement period I have so far spent $900 in foreign currency spending that were all contactless transactions as well. Do I need to top up $100+ in foreign currency spend to activate the 4 mpd rate, or is $100+ in local contactless transactions sufficient?

You must top up the foreign currency spend. $100 in foreign currency spend will activate the overseas transactions bonus and therefore unlock 4 mpd on all transactions to date in the statement period, however $100 of local payWave transactions is not sufficient to activate the bonus rate on all contactless transactions ($1,000+ local spend required), so in that case you’d still earn 0.4 mpd on everything.

Example 3: Within the statement period I have spent $1,200 on a hotel booking in foreign currency and $800 on local contactless purchases. With no other activity, will I get 4 mpd on all these transactions?

No – You will get 4 mpd on the $1,200 hotel booking but only 0.4 mpd on the remaining $800 contactless purchases, because you did not hit $1,000 in local spend. If you now spend a further $200 locally (whether contactless or not) you will get 4 mpd on the $800 contactless transactions and 0.4 mpd on the remaining $200 spend, because the monthly $2,000 limit for 4 mpd transactions had already been reached.

Example 4: My statement date is 15th May. If I spend $2,000 in foreign currency on 5th May and another $2,000 in foreign currency on 20th May, will I get 4 mpd on all $4,000 spend in the same month?

Yes – As both transactions are in different statement cycles, you will get 4 mpd on all $4,000 spend in this case. This assumes you have no other transactions on the card in either statement period.

Our strategy with this card is to keep it simple and use it only for foreign currency transactions, in (statement) months we know we can definitely transact between S$1,001 and S$2,000 in that category.

There’s nothing to stop you alternating between contactless transactions in one statement period and foreign currency ones in the next, but we don’t recommend trying to trigger both bonuses in the same statement as you’ll inevitably lose out on some miles at 0.4 mpd in order to guarantee each category ‘activation’, and in the worst case you might make a mistake and lose out on a lot of miles.

Posting date, not transaction date

For spend in the two bonus categories, it’s the date the transaction is posted to your account not the date the transaction was made that determines which statement month it is apportioned to.

For example if your statement period is 15th June to 14th July then you make a transaction on 13th July which posts on 16th July it will be considered a July / August statement transaction in terms of the ‘monthly’ minimum and spend cap.

UOB does not allow any leeway in this regard.

“UOB will not be liable for any late transaction postings affecting your eligibility to qualify for the bonus UNI$.”

Don’t forget that overseas transactions can take up to a week to post, so there is sometimes no way to know for certain which statement period they will post into.

How much is a UNI$ worth?

Anything from around 1 cent, when used to purchase gift vouchers or achieve cash rebates, through to 3.8 cents, when converted to KrisFlyer miles or Asia Miles.

Clearly the 1 cent option is unattractive, representing a poorer return than you would expect to achieve from many cashback cards, so we don’t recommend that.

Conversion into frequent flyer miles is the best deal.

Are KrisFlyer miles credited directly?

No, in fact rather than being credited miles directly you’ll accrue ‘UNI$’ for your regular spending on this card. These transfer to KrisFlyer miles at a 1:2 ratio (so for $1,000 of spending in the 4mpd (10X) bonus categories, you’ll net 2,000 UNI$, which converts to 4,000 KrisFlyer miles).

What is the transfer cost to KrisFlyer miles?

It will cost you $25 each time you transfer your points to KrisFlyer miles.

Auto conversion option

There is also the option to enrol in UOB’s auto miles conversion program, with payment of $50 per year. In that case your miles will be transferred automatically to KrisFlyer each month.

UNI$ will be converted at the end of each month in blocks of UNI$2,500 for 5,000 KrisFlyer miles.

A minimum balance of UNI$15,000 will remain in your account and must be maintained at all times.

That UNI$15,000 will not be auto converted to KrisFlyer miles. Only your UNI$ amount above UNI$15,000 will be automatically converted to KrisFlyer miles each month.

That means you’ll need at least UNI$17,500 in your rewards account for a transfer to take place. That’s not an attractive proposition for a card like this, which you’ll likely only be using for up to $2,000 of contactless or overseas transactions each month. It would be better to spend $25 each time for the transfer as you need it.

If you do wish to enrol in the auto conversion programme, the application instructions can be found here.

Is there a minimum transfer amount?

The minimum volume of miles you can transfer into KrisFlyer or Asia Miles is 10,000 (i.e. 5,000 UNI$), and they must then be in blocks of 10,000.

Do UNI$ expire?

Yes, your UNI$ expire 2 years after you earn them (by quarterly period). This is a downside to the UOB cards because many other banks tend not to have expiry rules for their loyalty points.

Remember your points will have a further three years validity once transferred to KrisFlyer miles, and will never expire if transferred to Asia Miles provided you earn or redeem at least 1 Asia Mile every 18 months.

How long do miles take to credit to KrisFlyer?

14 to 21 working days is the official period stated by UOB rewards, which implies that it might take over a month. If you had your eye on a redemption seat, it may be long gone by then!

Luckily the FlyerTalk forum post where KrisFlyer members share the actual number of days taken to transfer miles across from various banks, suggests that 1 to 3 days is more typical from UOB, with 7 days being the longest. That’s not the fastest on the market, but it is much more reasonable.

Which loyalty schemes can I transfer into?

Singapore Airlines KrisFlyer and Cathay Pacific Asia Miles.

![]()

The same earning rate, transfer cost, and minimum transfer ‘blocks’ apply if you choose to credit to Asia Miles.

Instant free transfer to KrisFlyer miles via KrisPay

You can also link your UOB Rewards and KrisPay accounts and instantly transfer as little as UNI$1,000 into KrisPay miles.

The transfer ratio is 1:1.7 (e.g. UNI$1,000 = 1,700 KrisPay miles).

You won’t want to be using them there due to the awful value against purchases of 0.67 cents per mile, but you can immediately transfer them 1:1 into your KrisFlyer account as KrisFlyer miles.

As you’ll notice this is a 15% ‘hit’ on the usual UNI$ to KrisFlyer transfer rate, so it’s only of interest if you need a small amount to meet a specific redemption threshold, or have a small balance ‘stuck’ in UNI$ (less than 5,000), which you aren’t going to be adding to in future.

You shouldn’t be using this as your regular UNI$ to KrisFlyer transfer method, as it effectively devalues your miles earning rate to 1.19 mpd locally and 2.04 mpd for FCY purchases.

There are two golden rules to be aware of, firstly you’ll have to move any points transferred from UNI$ to KrisPay into KrisFlyer miles within seven days, otherwise they are stuck in KrisPay (where you definitely don’t want them).

The second is just as important, you cannot use any of the KrisPay miles you have earned from your UNI$ transfer for any KrisPay purchase, no matter how small, as that automatically renders the entire transfer stuck in KrisPay until they then expire.

The golden rule therefore is to transfer in to KrisPay, then transfer straight out to KrisFlyer. Even with that seven-day window available, our advice is don’t wait.

Points rounding

One big drawback of UOB credit cards is that UNI$ are awarded for every $5 block of spending charged to your card.

When you are charging smaller amounts, that does start to have a big impact on the effective miles per dollar rate you are actually earning for the transaction.

| UNI$ awarded | ||

| Charge | General Spend | Bonus Category Spend |

| $4.99 | 0 (0 mpd) |

0 (0 mpd) |

| $5.00 | 1 (0.4 mpd) |

10 (4 mpd) |

| $9.99 | 1 (0.2 mpd) |

10 (2 mpd) |

| $10.00 | 2 (0.4 mpd) |

20 (4 mpd) |

One cent can make all the difference here, and to truly optimise the maximum number of UNI$ earned, you should plan your spending in $5 blocks especially at the lower transaction levels (e.g. $5 / $10 / $15).

Try to avoid falling just below a $5 block if possible, or only exceed a $5 block by a small amount.

The impact becomes less important with higher amounts, for example let’s say you make a valid overseas transaction with your UOB VS card having activated the overseas spend bonus category:

- $249.99 – 490 UNI$ awarded (980 miles / 3.92 mpd)

- $250.00 – 500 UNI$ awarded (1,000 miles / 4 mpd)

As you can see falling 1 cent short of a $5 block size in this case isn’t significantly affecting your miles per dollar rate in the same way that a $9.99 vs. $10.00 spend is.

As individual transaction amounts increase further, the effect becomes even more negligible.

UNI$ pool with your other cards

If you earn UNI$ through an existing credit card account, such as the UOB PRVI Miles card, your points balance will be pooled together into a single balance for you to redeem from.

If you cancel your card, any UNI$ accrued will survive in your ‘pool’ provided you still have at least one other UOB credit card earning UNI$.

Minimum spend to earn points

With no UNI$ awarded for transactions below $5, the minimum spend to earn points is of course $5.

Smaller transactions, including those converted from foreign currency into SGD which are charged to your card at less than $5, will not earn any points.

Foreign currency fee / cpm overseas

One thing you won’t be wanting to do with this card is make transactions in foreign currency at the basic 0.4 mpd earn rate.

With UOB’s 3.25% foreign currency fee, that’s equivalent to ‘buying’ miles at an obscene 8.57 cents each, way more than you can ever realistically achieve in value.

At the 4 mpd bonus rate though, which would apply for example on foreign currency transactions of $1,000 – $2,000 in the same statement period, the equation means buying miles at 0.86 cents each, an excellent rate to accrue them.

Here’s how that cost per mile compares to other credit cards in Singapore offering 4 mpd for at least some form of eligible transactions in foreign currency.

Cost per mile on overseas credit card transactions (4 mpd cards)

(Best to worst, May 2020)

| Card | Fee | Miles per $ | Cost per mile |

| 3.25% | 4.0 | 0.86¢ | |

| 3.25% | 4.0 | 0.86¢ | |

| 3.25% | 4.0 | 0.86¢ | |

| 3.25% | 4.0 | 0.86¢ | |

| 3.25% | 4.0 | 0.86¢ |

Cost per mile also accounts for an additional 0.3% ‘spread’ over money changer currency rates, though this doesn’t apply to all banks and all foreign currencies, so is a worst-case scenario.

As you can see with the same 3.25% foreign transaction fee across all these cards, the UOB Visa Signature card matches the others.

Complimentary Travel Insurance

If you charge your UOB VS card with your entire fare for travel by “air, land or water

conveyance”, you’ll qualify for complimentary travel insurance, which includes the

following benefits:

Travel Personal Accident Insurance

Covers accidental death or disablement whilst on public conveyance:

- Up to S$500,000 for you

Emergency Medical Assistance, Evacuation and Repatriation

- Up to S$50,000 for you

The specific terms, conditions and exclusions applicable to this travel insurance are set out in the Insurance Certificate and Agreement.

Other benefits

The UOB VS card isn’t showered with an abundance of other benefits. The key additional ones which will be of most interest to our readers are:

- 1 UNI$ (2 miles) per $5 spend on SimplyGo transit rides, based on the accumulated spend on SimplyGo Transactions per calendar month, and awarded to Cardmembers on the 7th calendar day of the following month (details here). Note that with this promotion you must register your UOB VS card with SimplyGo then charge the journeys to your Transit Card via your mobile phone using Apple Pay, Fitbit Pay, Google Pay and/or Samsung Pay, do not simply tap the card.

- A range of Dining Promotions common to all UOB cards.

- UOB Privileges Passport, including up to 10% cashback at Booking.com and 8% off Hotels.com bookings.

Our summary

The UOB VS card is a relatively easy way to earn 4 mpd on a range of transactions each statement period, however the shared $2,000 spend cap across two bonus categories, each of which require a minimum $1,000 spend to activate, makes it impossible to utilise this higher rate in all the bonus categories (overseas, petrol and contactless) without inevitably overspending at the lousy 0.4 mpd rate.

The key to this card is to just stick to one of the bonus categories (either overseas spend or petrol / contactless spend) and make sure your transactions fall within the $1,000-$2,000 bracket each statement period.

With a $2,000 limit each month, this can potentially net you 96,000 miles per year with relative ease, more than enough for two people to fly Business Class on SIA from Singapore to Tokyo or Seoul.

Remember we value KrisFlyer miles at around 1.9 cents each, so at the 4 mile per dollar rates you’re earning close to 8% ‘value back’ on your purchases.

Outside the bonus rates, it’s a very poor earning rate on this card of 0.4 miles per dollar, so we would strongly recommend having an alternative for your day to day spending where you should be earning at least 1 mile per dollar, and ideally 1.2 to 1.5 miles per dollar.

This is especially important if you exceed the $2,000 bonus cap each month.

Another drawback of this card to be aware of is the two-year validity period for UNI$ accrued, so do make sure you transfer your points into KrisFlyer or Asia Miles in good time.

(Cover Photo: Saranya Phu Akat / Shutterstock)

Hi Andrew, thanks for the helpful information. To be absolutely sure, I wish to clarify – if I were to make an online payment to a SG merchant (assuming not on exclusion list) via ApplePay on my iPhone, will that qualify as part of the $1,000-2,000 local spend?